Chart: Why China’s solar boom is slowing down

Solar power has been a major element of China’s renewables buildout since the mid-2010s.

The country installed 315 gigawatts (GW) of new capacity in 2025, adding more than half of all new solar globally. The year before, it added 277GW.

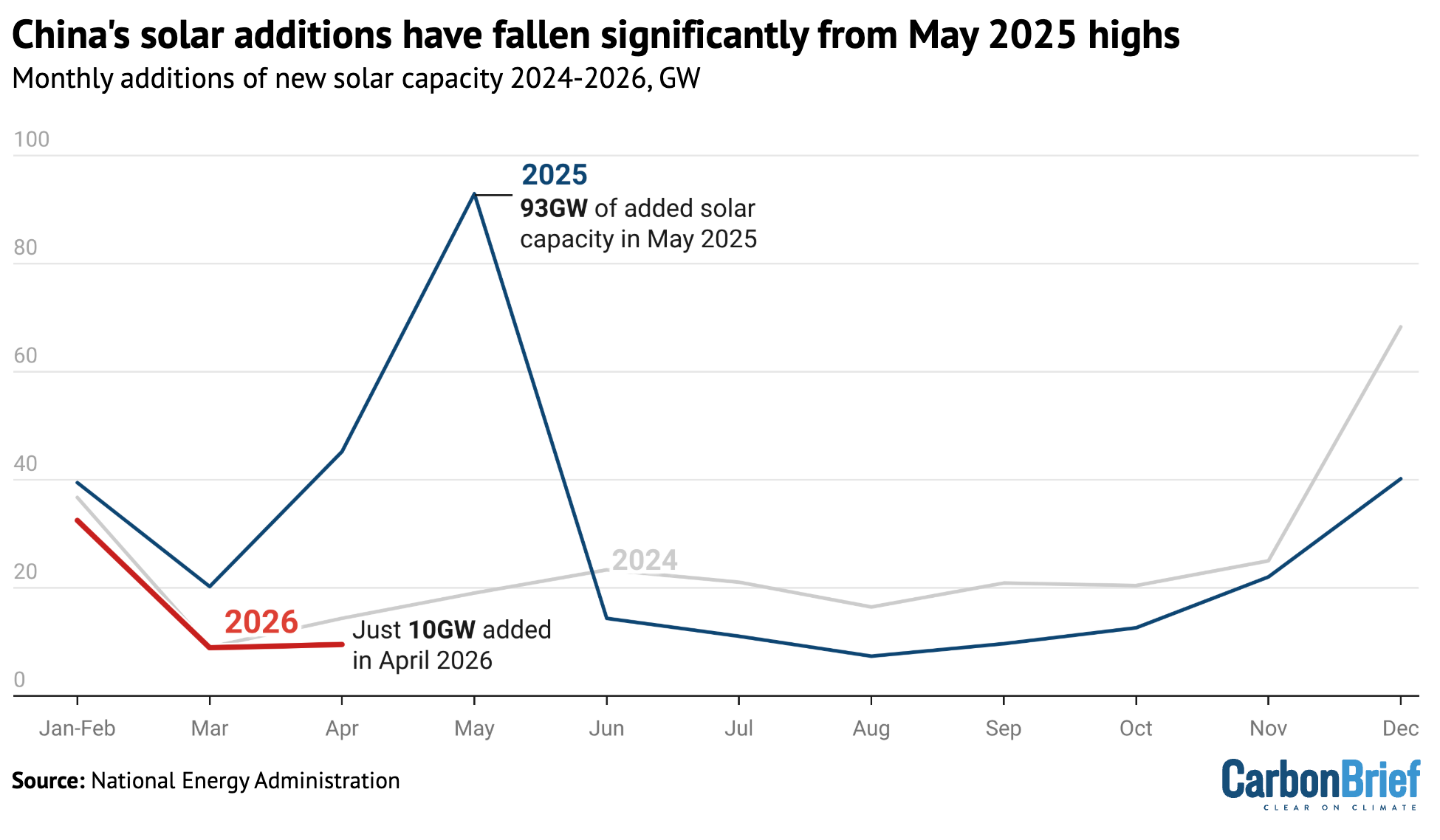

But the picture in 2026 to date is very different. Installations in March fell 56% year-on-year to 9GW, while new capacity in April totalled 10GW, a 79% drop compared to a year earlier, according to Carbon Brief’s analysis of official data.

{kind=link}

§ Domestic uncertainty

The lower pace in 2026 had been anticipated by analysts.

In previous years, massive solar installations were driven by strong policy support for renewables, including a fixed-price tariff for generators.

In February 2025, the government announced that new solar and wind projects would instead be financed through a new “contract for difference” (CfD)-style system.

Under the new system, power from a certain amount of renewable capacity will be purchased for a fixed “strike price”, which to date has been far lower than previous guaranteed tariffs. Further projects will need to secure their own contracts on the open market.

While the new system is posing challenges for developers in the short term, it is part of a longer-term shift towards market-driven pricing for renewables, which has already made them cheaper than coal.

The change led to a rush of new project installations ahead of the June 2025 cut-off date, so that they could fall under the old fixed-price regime.

New solar additions totalled 45GW in April 2025 and 93GW in May 2025, before falling to 14GW in June 2025, according to Carbon Brief analysis of government data.

Additions also spiked in December, in both 2024 and 2025, as developers raced to meet completion deadlines including those under the 14th five-year plan.

Some reports have attributed the precipitous drop this year to falling demand for solar in China.

But this is a “major oversimplification”, David Fishman, principal at energy consultancy the Lantau Group, wrote on LinkedIn.

The real challenge, he said, is that “developers and banks [are] still figuring out how to finance and build projects without policy-backed revenue guarantees”.

Yang Biqing, energy analyst for Asia at thinktank Ember, agrees, telling Carbon Brief that the new CfD-style system has created “greater uncertainty” for developers, compounded by fierce competition and a growing push for “consolidation” in the industry.

The government set a target for 200GW of new solar and wind capacity in 2026.

Fishman tells Carbon Brief that this will be “difficult” for the government to achieve, though not impossible. Current levels of solar additions – reaching perhaps 120GW for the year – plus an “ambitious” 80GW of new wind power, could help China to hit the target, he says.

Others are more bullish. The China Photovoltaic Industry Association forecasts 180-240GW of new solar in 2026.

But few believe additions will match the breakneck pace of 2025.

“China’s solar industry is no longer a story of capacity expansion”, says Yang, with officials now “increasingly” focused on integrating current generation into the grid.

§ Soaring exports

Meanwhile, China’s solar exports are still going strong.

China exported almost 1.2m tonnes of solar cells in April 2026, according to Reuters. Although down from a record high in March, it represented a 60% rise year-on-year, added the newswire.

This signals solar’s attractiveness globally in the face of rising energy prices caused by the Iran-US conflict, analysts have said.

High demand for panels has been reported across several continents, including Europe, Asia and Africa.

For example, in the Philippines, the conflict is “driving” solar uptake, one analyst told the Associated Press, adding:

“People want solar and people want solar now.”